TFI Tax Facts (78.2): Illinois’ Personal Property Replacement Tax: History, Volatility and the Road Ahead

Illinois’ Personal Property Replacement Tax: History, Volatility and the Road Ahead

fffffffff

December 2025 (78.2)

Executive Summary

Illinois’s Personal Property Replacement Tax (“PPRT”) is a uniquely structured revenue source that remains poorly understood despite its fiscal importance. Most PPRT revenues1 are derived from taxes on business income, making them inherently volatile and sensitive to economic and policy changes.

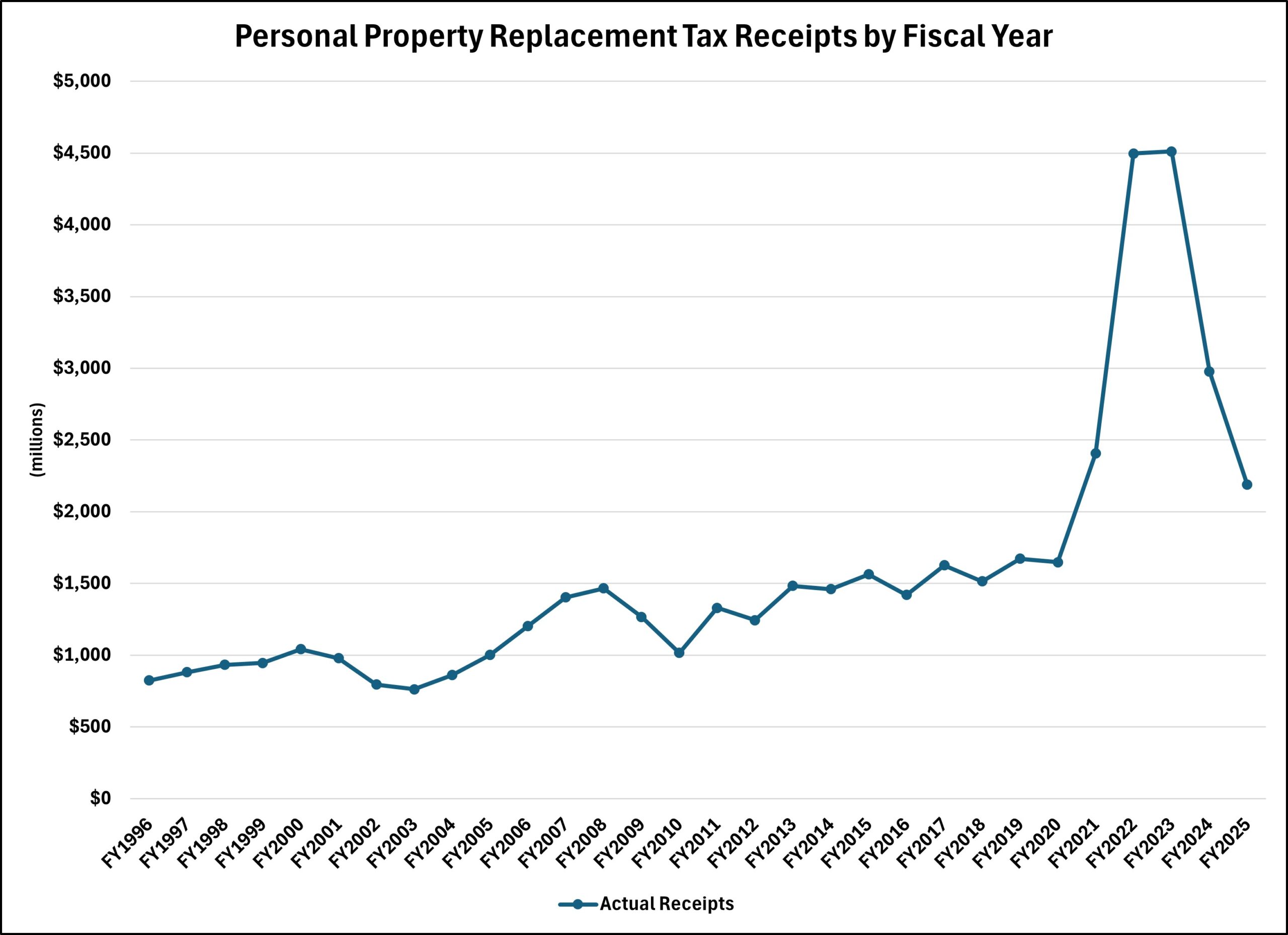

After reaching unprecedented highs in State Fiscal Years 2022 and 2023, PPRT revenues have since declined, largely due to the correction of a multi-year over-allocation tied to the introduction of the Pass-Through Entity Tax (“PTET”). Local governments have seen lower distributions in SFY2024 and SFY2025 as the state implements “true-up” adjustments and multi-year recovery measures. While the correction process has created short-term volatility, underlying PPRT collections remain historically strong and are expected to continue growing over time.

Understanding how Illinois replaced its former personal property tax, how the PTET disrupted long-standing allocation patterns, and how current formulas are being realigned provides important context for local governments and policymakers planning future budgets.

This article explains the structure of PPRT, the causes of recent fluctuations, and what to expect going forward as Illinois works to restore equilibrium in this critical revenue stream.

How Illinois Replaced its Personal Property Tax

Illinois was one of 14 states in 2025 without a tax on personal property, according to the Tax Foundation. However, Illinois had a personal property tax until 1979. Previously, Illinoisans paid taxes based on the value of tangible goods, such as vehicles, equipment, equities, and livestock, that were not subject to real property taxes. The personal property tax was unpopular and riddled with barriers to effective administration. For example, investors transported their stock and bond certificates across state lines so they were not in Illinois on assessment dates.

The State of Illinois transitioned away from real and personal property taxes in the 1930s, but local governments in Illinois continued to rely on them. Cook County stopped imposing personal property tax on individuals in 1950 but continued to tax personal property owned by a business. The personal property tax on individuals was abolished in 1969 as part of the Illinois income tax enactment, and voters adopted a new state constitution a year later that mandated the abolition of the personal property tax on businesses by January 1, 1979.

However, the new constitution also required lawmakers to establish a suitable replacement revenue source to offset the local government revenue loss. The constitution said the replacement was to fall “solely on those classes relieved of the burden of paying ad valorem personal property taxes because of the abolition of such taxes. . .” Lawmakers struggled throughout the 1970s to reach consensus on a suitable replacement and even proposed a failed constitutional amendment that would have reversed the personal property tax abolition. They eventually settled just before the 1979 deadline on a package of taxes – the Personal Property Replacement Tax – to meet the constitutional requirement, specifically:

– A 2.5% corporate income tax (it was slightly higher the first year).

– A 1.5% tax on the net income of partnerships, Subchapter S corporations, and trusts.

– A 0.8% tax on the invested capital of public utilities.

When telecommunications and electric utilities were deregulated in 1998, the electricity excise tax and telecommunications infrastructure maintenance fees replaced the tax on capital investments within those industries, except electric cooperatives. The income tax portion generally produces 85% of the PPRT revenues.

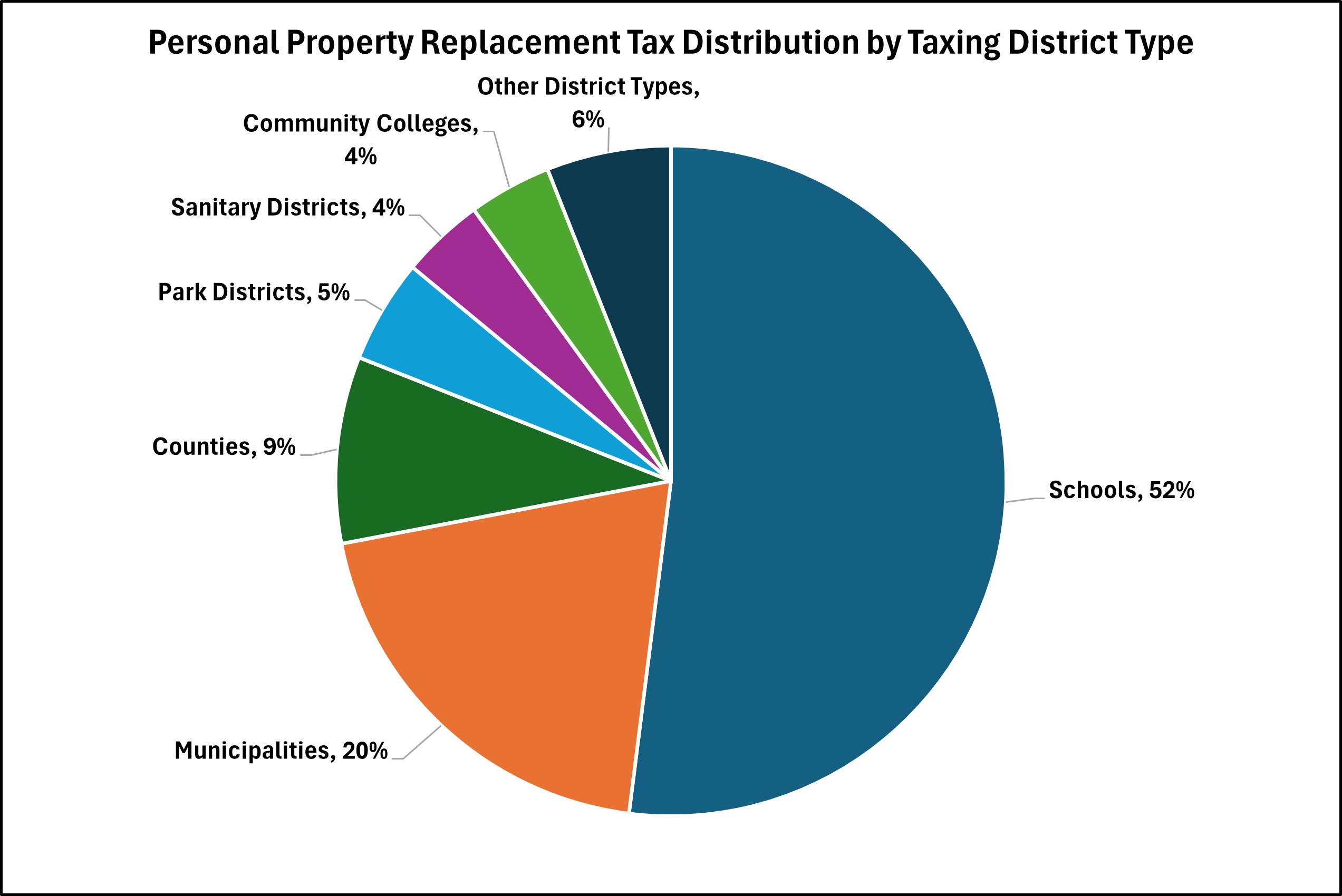

Taxes are collected by the Illinois Department of Revenue (“IDOR”) and distributed based upon historic personal property tax collections, with 51.65% going to local governments in Cook County and the remaining 48.35% going to local governments outside of Cook County. Each local government distribution is based on its share of personal property replacement tax collected in 1976 for those in Cook County and 1977 for the rest of the state. Since PPRT distributions are tied to the collection of personal property tax revenues from the 1970s, taxing districts with substantial population and economic growth since then often receive a disproportionately smaller share compared to districts with little growth or population declines.

Source: Illinois Department of Revenue

IDOR distributed $1.98 billion in PPRT to 6,488 local governments in SFY2025. These distributions ranged from $278 million for Chicago Public Schools to $7.09 for the McConnell Street Lighting District in Stephenson County. The median annual payment was slightly less than $10,000.

PPRT Overallocation Leads to Multi-Year Claw Back

The creation of the pass-through entity tax significantly altered taxpayer payment patterns, yet allocation formulas for the PPRT continued to rely on historical trends. This mismatch between new payment behavior and legacy modeling resulted in an estimated $2.1 billion over-allocation of PPRT revenues, which the state is now addressing through multi-year adjustments and repayments.

Source: Illinois Department of Revenue

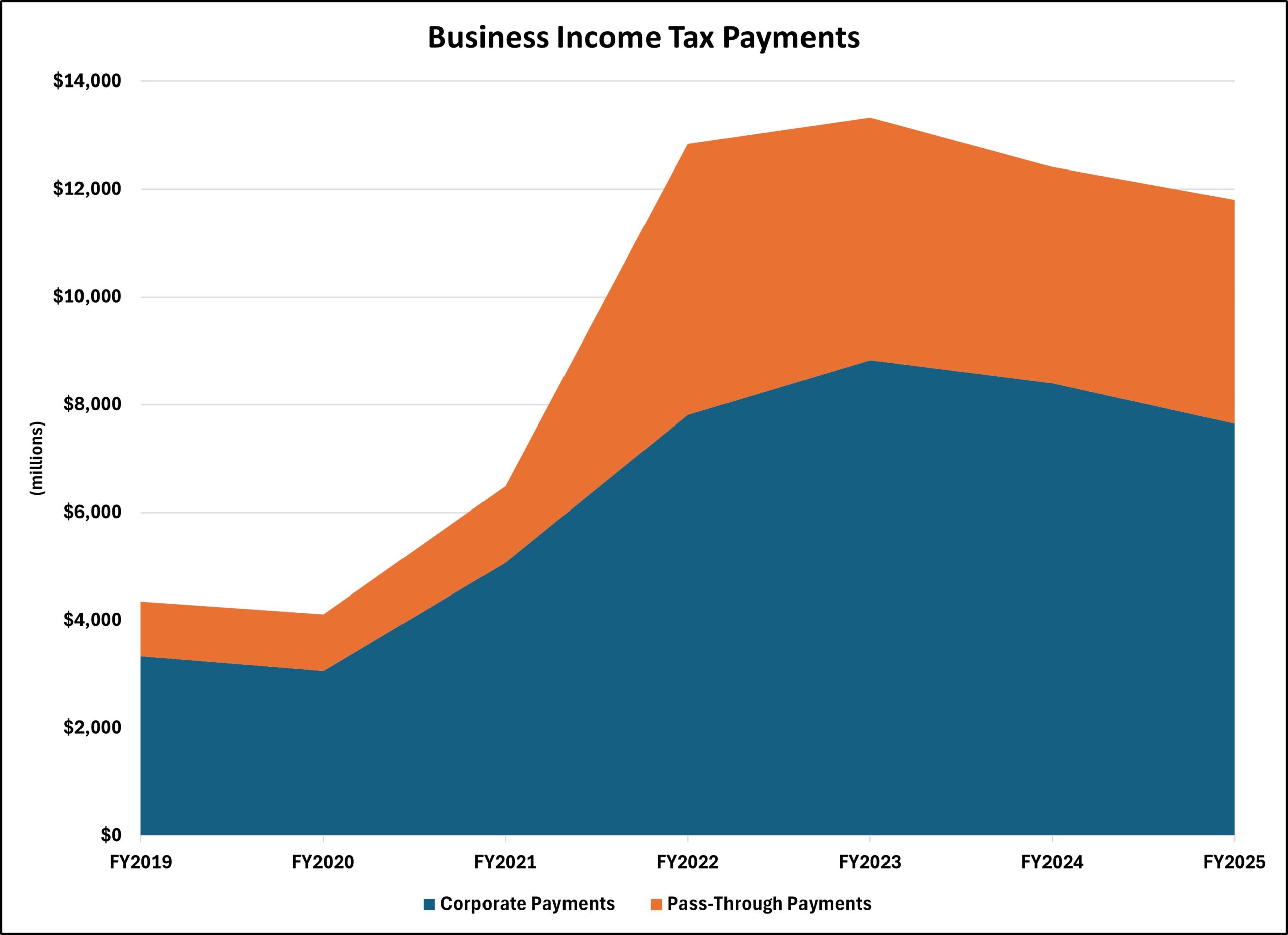

Illinois enacted the Pass Through Entity Tax (P.A. 102-0658) on August 27, 2021 in response to the federal Tax Cuts and Jobs Act of 2017, which capped the state and local tax deduction at $10,000 for individual taxpayers. The PTET allows partnerships or S corporations to pay the Illinois individual income tax on their owners’ share of business profits directly. If the business pays the tax, then the business owner receives an Illinois income tax credit equal to the tax paid. The business deducts the tax payment on their federal return, thereby getting around the $10,000 cap. The PTET is estimated to have saved Illinois taxpayers about $500 million in federal income taxes per year since 2021. To date, more than 35 states have passed similar PTETs.

After the PTET took effect and taxpayers began realizing its benefits, tax payments from pass-through entities increased from $1.4 billion in SFY2021 to $5.0 billion in SFY2022.

Source: Illinois Department of Revenue

Historical Data Fails to Account for New Normal

Shortly after a taxpayer makes a tax payment to the State of Illinois, IDOR is required to determine what tax type the payment is for, place the money into the proper state fund, and queue distributions to state and local government units. State law provides different distribution formulas for different taxes. When IDOR receives an income tax payment, they need to determine to the best of their ability whether the payment is for PPRT, corporate income tax, or individual income tax. The determination by IDOR needs to happen immediately even though the taxpayer may not file their income tax return for another year or longer.

Because of the time between when tax payments are made and when tax returns are processed, IDOR uses historical data to predict how the payments should be allocated between PPRT, corporate income tax, and individual income tax. When income tax returns are finally received and processed, IDOR calculates how the earlier payments should have been allocated and then transfers funds to reflect the final allocation. This is informally known as the “true up” process. Prior to 2021, the typical annual true up was about $20 million.

When the PTET was enacted in 2021, the allocation framework for business income taxes continued to rely on historical patterns. Payments received through SFY2023 were distributed according to pre-PTET methodologies, with each deposit classified as it would have been prior to the new tax. For example, every payment made by a partnership in SFY2021 was allocated as follows:

– 9% of each payment was allocated for corporate income tax liabilities.

– 33% of each payment was allocated for PPRT liabilities.

– 57% of each payment was allocated for individual income tax liabilities.

After processing all Tax Year 2021 tax returns, IDOR determined in spring 2023 that payments from partnerships should have been allocated differently:

– 6% of each payment should have been allocated for corporate income tax.

– 23% of each payment should have been allocated for PPRT.

– 71% of each payment should have been allocated for individual income tax.

Payments that were allocated as corporate income tax but should have been distributed as individual income tax was not an overly significant concern, as their distribution formulas are similar and the majority of the revenues go to the State’s general funds, but adjustments were still made. However, the overallocations benefitting PPRT at the expense of individual income tax were a much larger concern since those revenues are distributed to different government units.

This same true up process had to be performed for payments from each business entity type. In the spring of 2023, IDOR identified $704 million2 which was overallocated to PPRT, which should have been individual income tax. To correct the overallocation, IDOR did two things:

– Change the allocation percentages for corporate income tax, individual income tax, and PPRT for tax payments that would be received in SFY2024.

– Claw back the $704 million PPRT over-payment from SFY2024 PPRT collections.

These two simultaneous changes created a double whammy for local governments and were the overwhelming factors in the $1.533 billion decrease in PPRT revenues from SFY2023 to SFY2024.

IDOR announced in spring 2024 a similar true-up for SFY2025 as PPRT had been overallocated by an $879 million. Updating that allocation formula and the $879 million in claw backs led to a further decline in PPRT revenues available for local government distributions.

More claw backs from PPRT to correct the overallocations are under way as part of the tax year 2023 true-up process, but there is a light at the end of the tunnel as changes to the allocation formulas are working through the system.

IDOR determined in spring 2025 the claw back for SFY2026 would be $538 million. While still sizable, it is $342 million less than the SFY2025 claw back. The less money that needs to be clawed back, the higher the PPRT distributions to local governments will be. A $342 million decrease in the claw back by itself represents a 15.6% over-the-year increase, assuming everything else is constant. However, in the real world, things are constantly changing, which means PPRT collections may increase or they may decrease.

Had there been a way to determine the correct allocation ratios when the PTET was created, eliminating the need for the $879 million claw back in SFY2025, there would have been $3.1 billion in PPRT collections that would have been available for PPRT purposes.

Source: Illinois Department of Revenue, Calculations performed by TFI

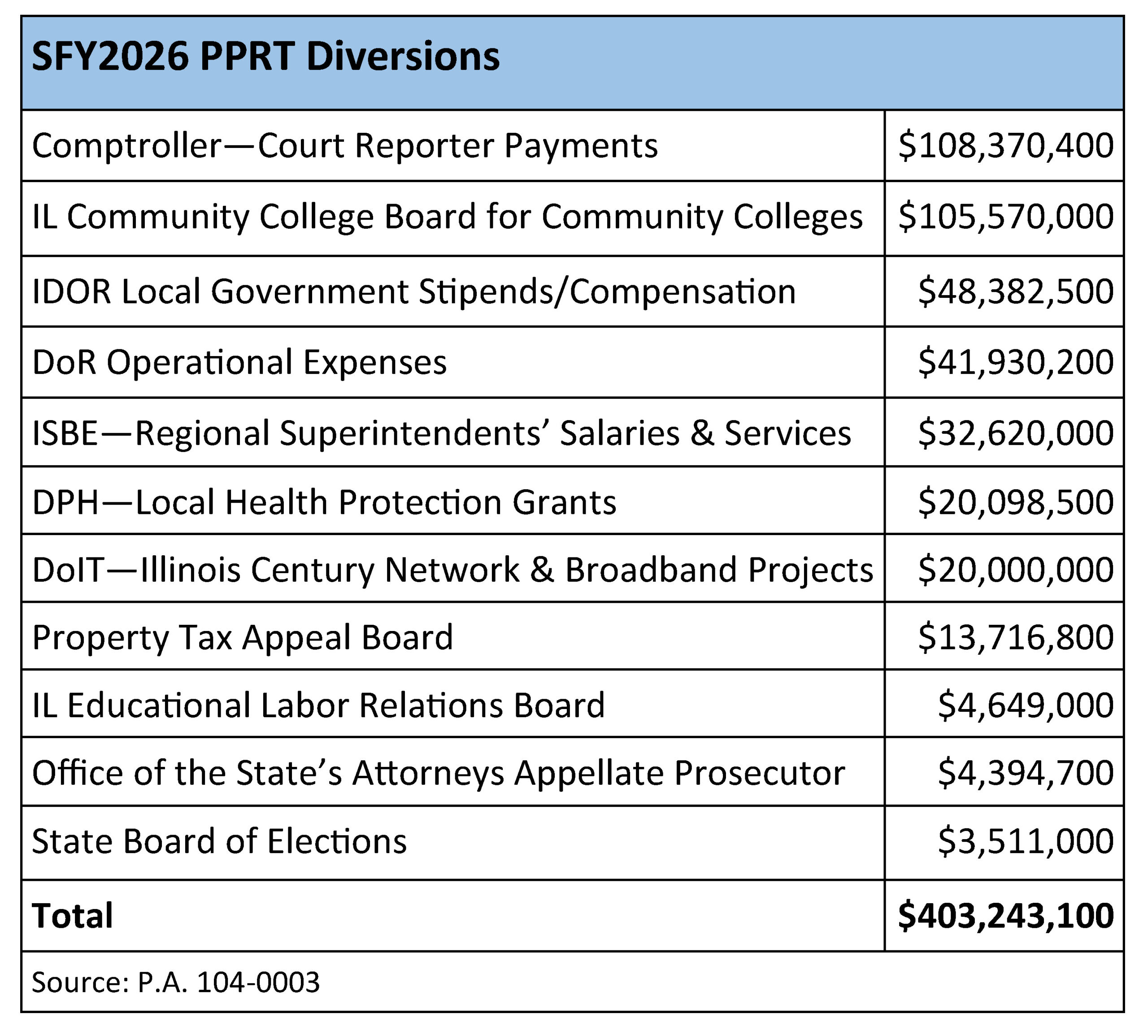

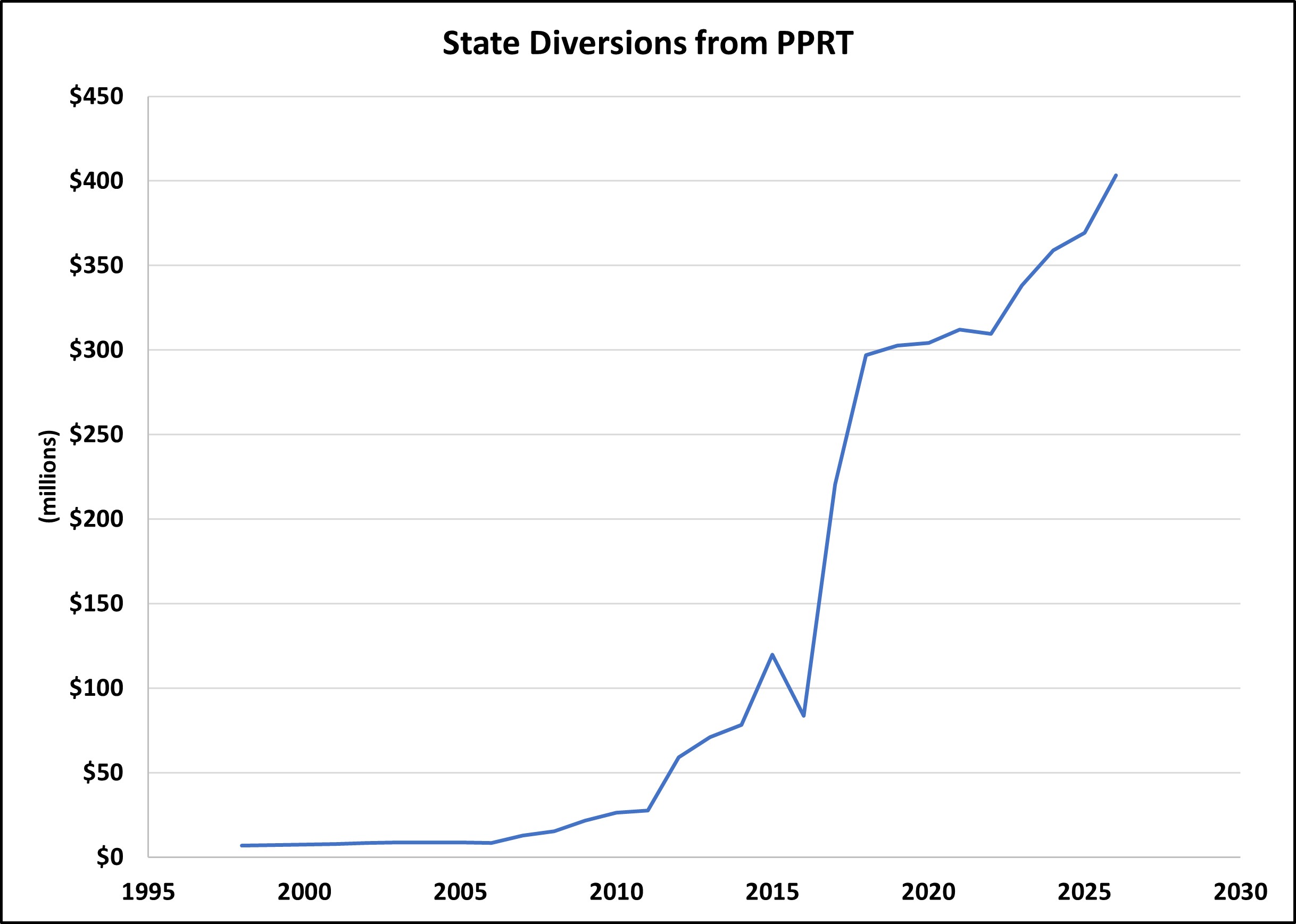

PPRT Diversions to Illinois State Government

Illinois lawmakers over the past 10 years have increasingly diverted PPRT revenues away from being distributed to local governments.

Though PPRT revenues were initially exclusive to local governments, state legislators and governors since 1997 have budgeted money from the PPRT Fund to pay for services they say benefit local governments. Before these budgeted diversions, most of these services were paid out of the state government General Funds. Citing difficult budget years in numerous instances, state lawmakers have identified additional expenses to pay using PPRT revenues, thereby reducing the amount of money available for distribution to local governments.

PPRT diversions to state government spending saw the largest increase in SFY2017 and SFY2018. However, diversions continued in the following budget years, but the unprecedented PPRT revenue growth made additional diversions more politically acceptable. In SFY2025, state diversions from PPRT were 16.9% of all PPRT collections. While PPRT revenues are expected in SFY2026 to increase, the State of Illinois operating budget includes $34 million in new diversions that will further reduce PPRT revenues.

Source: Illinois Department of Revenue

Conclusions

The introduction of the Pass-Through Entity Tax fundamentally altered how business income taxes flow into the state’s revenue system, causing overallocation of revenues to PPRT. The resulting two-year overallocation temporarily inflated PPRT receipts in SFY2022 and SFY2023, followed by significant claw backs in subsequent years as the formulas were corrected.

Although these adjustments have created short-term volatility for local governments, the underlying revenue base tied to business income taxes remains strong. With updated allocation models now in place, future PPRT distributions should better reflect actual taxpayer behavior and return to a more predictable trajectory.

Looking ahead, continued transparency and timely communication around allocation changes will be essential to rebuilding confidence among local governments that rely on this critical funding source. As Illinois’s economy evolves, maintaining a stable and well-understood PPRT framework will remain vital for local governments in Illinois.

Footnotes:

1 “PPRT Revenues” mean the amount of PPRT collected in a fiscal year, which is not the same as how much PPRT was distributed to local governments as there is a one month lag from collection to distribution and it does not reflect diversions.

2 True up amounts are based on the amount redirected from the Personal Property Replacement Tax Fund and does not include redirected amounts from the Income Tax Refund Fund.